ARX Series 12 November 2021

China's Pension Market

Progress Towards High-Quality Development

A presentation by Mr. Su Gang, Board Chairman of Changjiang Pension Insurance, in the second installment of the CFA Institute China Live Pension Management Series, "Pension and Climate Change: A China-Japan Dialogue.”

Introduction

The topic of my presentation is the Continuing high-quality development of China's pension market. It is specifically divided into three parts. The first part introduces some of the progress and achievements that have been made in China's pension market; the second part talks about the major challenges China currently faces in the development of its pension market; the third is a reflection on some of the paths to promote the high-quality development of China's pension market.

The Achievements of China's Pension Market

The Chinese pension market has seen 30 years of development since 1991. China's pension market has achieved remarkable results in the past 30 years. It is demonstrated specifically from the following four aspects:

First of all, this market has received great attention from the nation’s top leaders. The nation’s long-term plan to actively respond to aging population, the “Accelerating the Improvement of the System of Socialist Market Economy in a New Era,” and the 28th collective study session of the Central Political Bureau of the Communist Party of China earlier this year, as well as the latest outline of the 14th Five-Year Plan for National Economic and Social Development and Long-Range Objectives for 2035, have all reaffirmed the development of a multi-tiered and multi-pillar endowment insurance system and to actively implement the national strategies to cope with an aging population.

The second is the continuous improvement of the entire system. In the past 30 years, the pension plan has been established with enterprise annuities and occupational annuities for government agencies and institutions while having the basic government pension as a supplementary and since 2018, it has been explored that pension plans invested by individuals could be the third pillar of a more comprehensive pension plan.

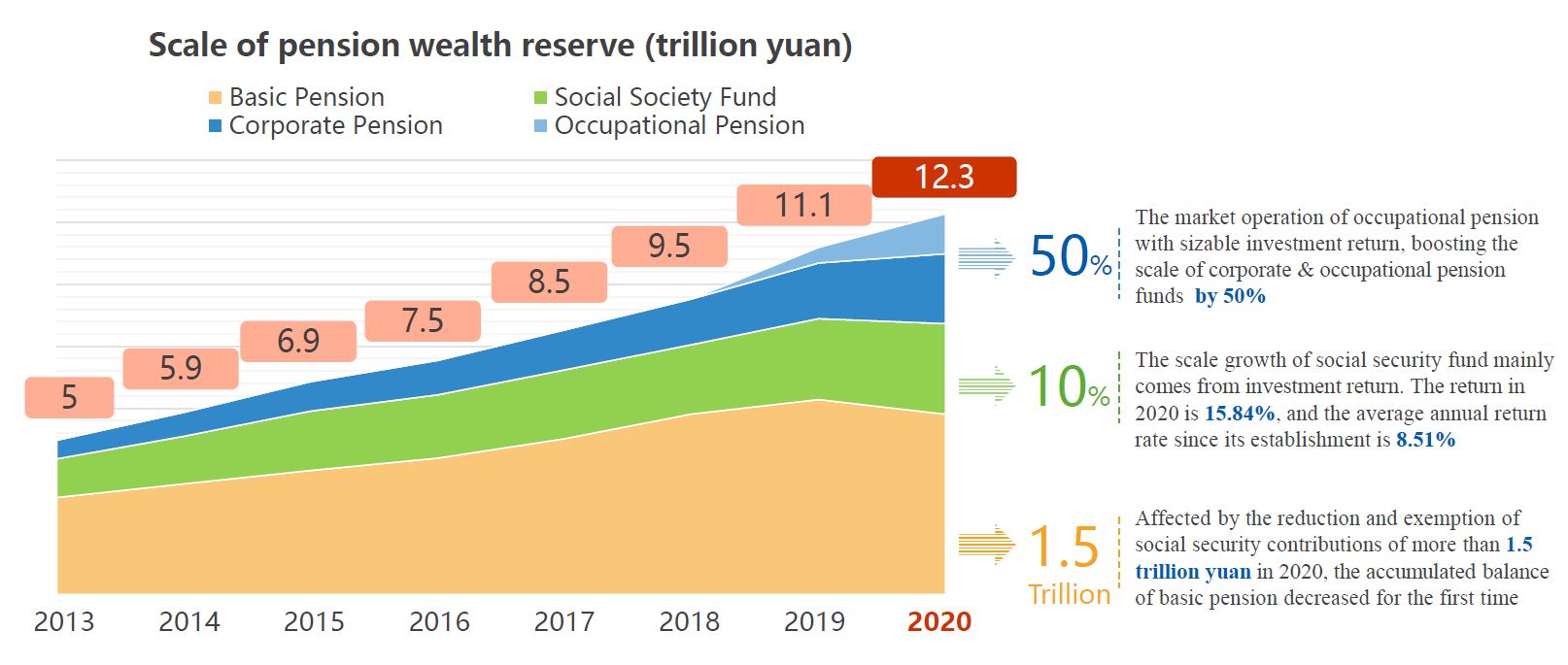

The third is the rapid growth of the entire Chinese pension market size. Starting from RMB 5 trillion in 2013, the total institutional pension reserves have now exceeded RMB 12 trillion, which include basic endowment insurance fund, social security reserve funds, enterprise annuities and occupational annuities.

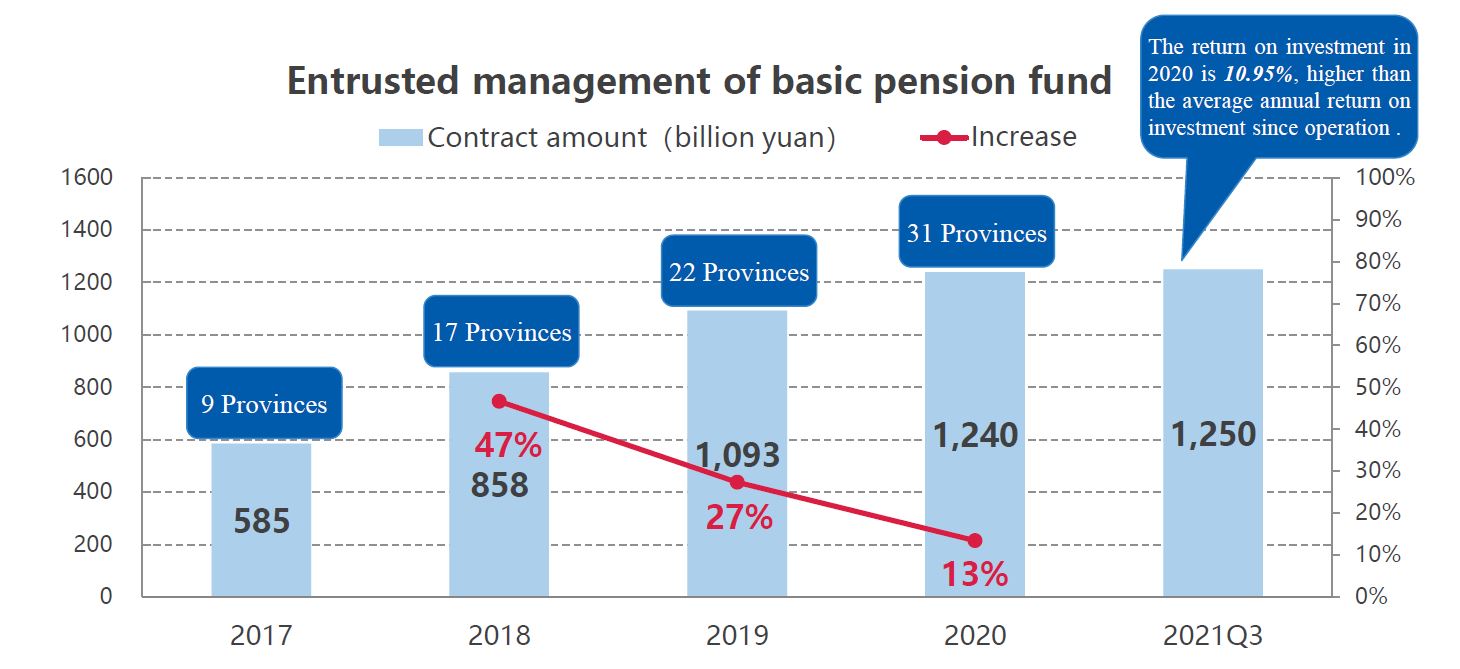

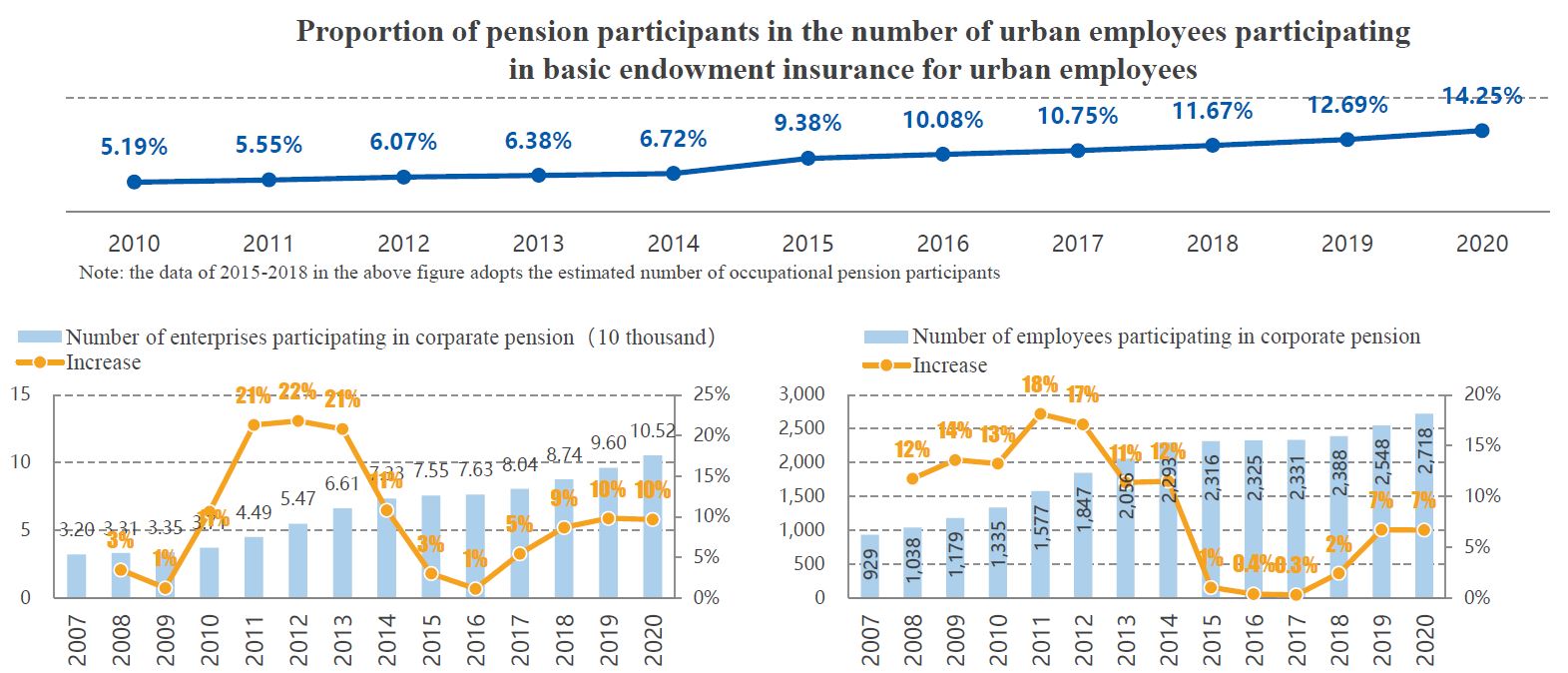

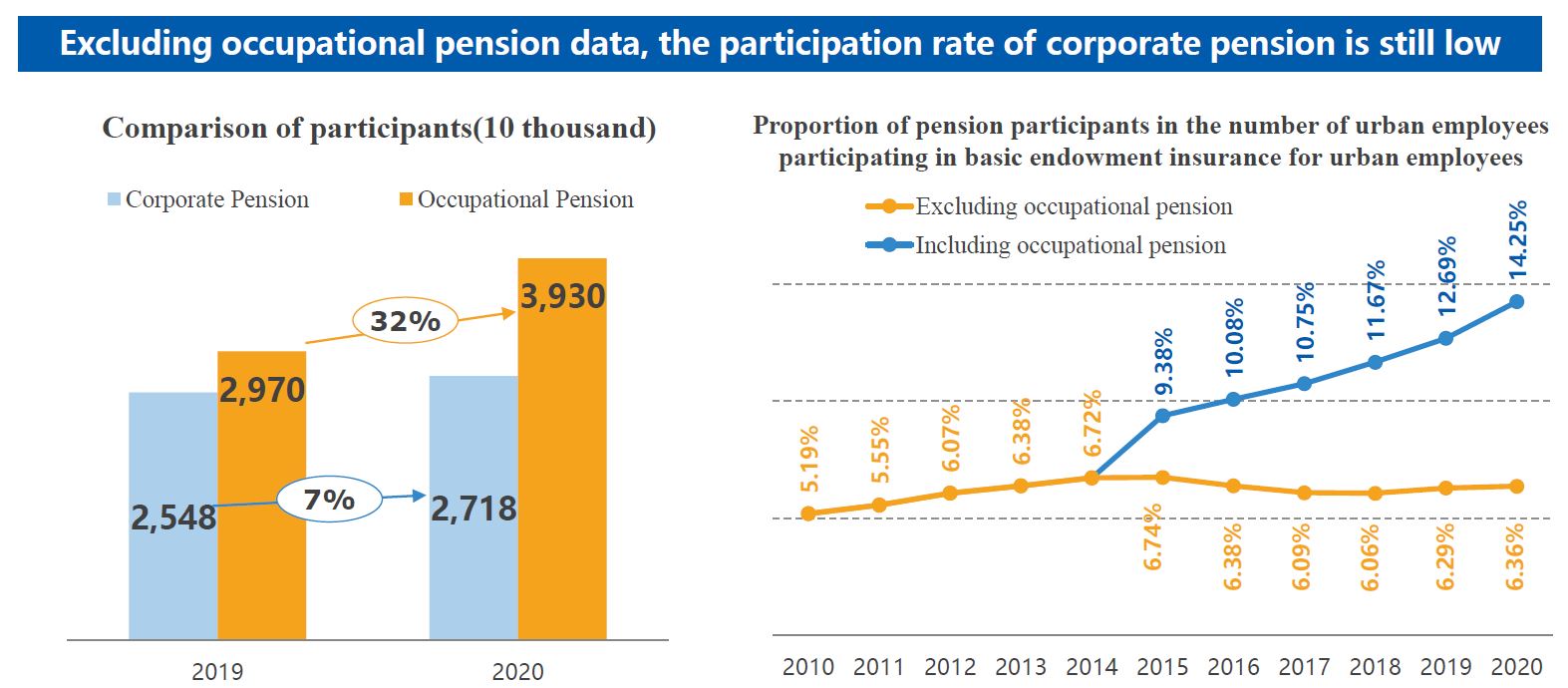

Of which, we have noticed that the first pillar of basic endowment insurance fund has now covered 31 provinces, with entrusted funds amounting to RMB 1.25 trillion. The second-pillar pensions have seen a significant increase in the proportion of annuities, from 12% of institutional pensions in 2013 to nearly 30% at present. Of course, one of the important influencing factors is the occupational annuity.

We can see that in the development history of annuities, the proportion of enterprise annuities has been hovering at about 7%. The launch of occupational annuities has not only driven the overall annuity proportion of institutional pensions to over 14%, but also promotes the gradual recovery growth of enterprise annuities since 2018.

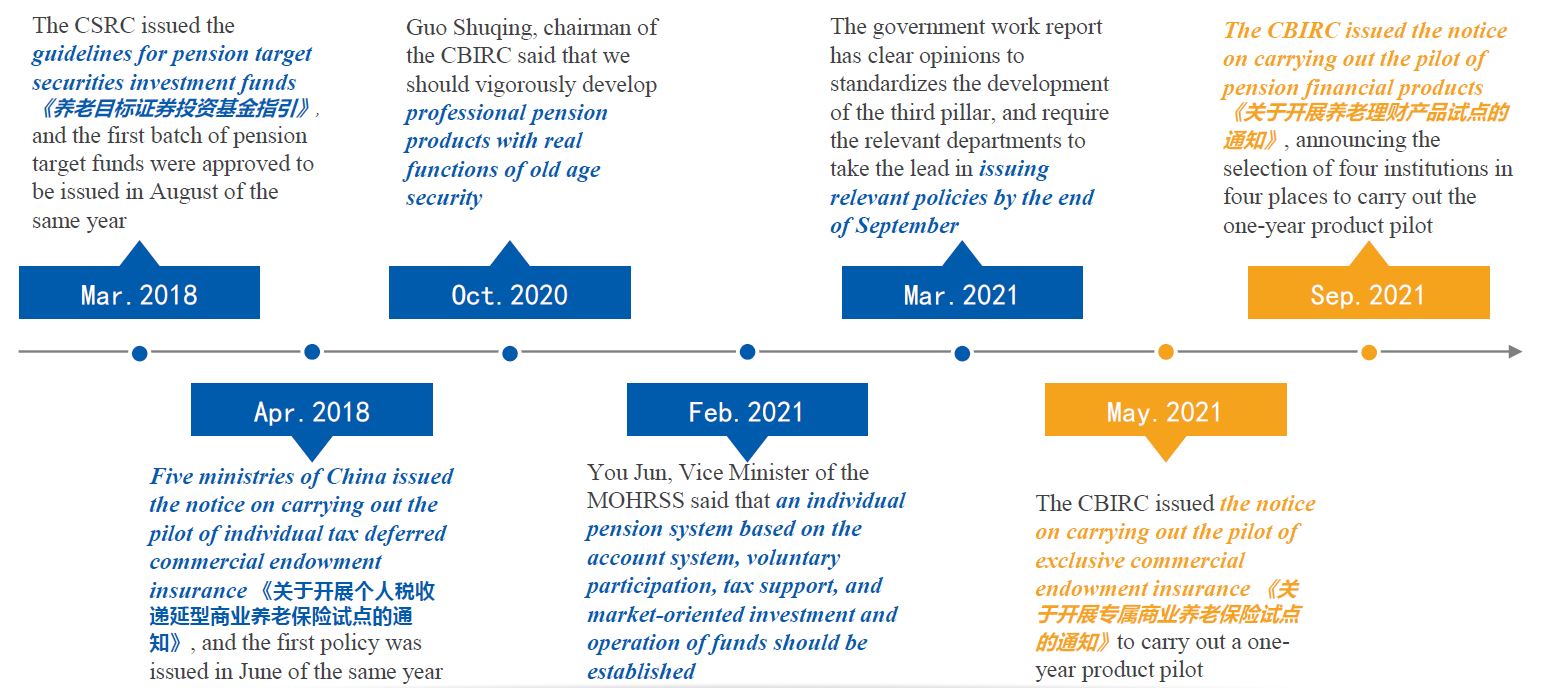

In terms of the third pillar, the entire system is being actively explored since 2018, and new products to support the third pillar of the pension system in various areas, including individual tax deduction, [tax-]deferred commercial pension insurance, pension target funds, financial products for pension, and exclusive commercial endowment insurance are being actively identified. At present, we are looking forward to the introduction of the new top-level system design as soon as possible.

Fourth, there is an evident trend of inter-industry competition. Financial institutions holding various subdivision licenses of pension management are among insurance companies, banks, funds, securities, and trusts, which can be said to cover all the leading institutions related to pan-asset management.

Major Challenges in China's Pension Market

Specifically, there are three prominent aspects:

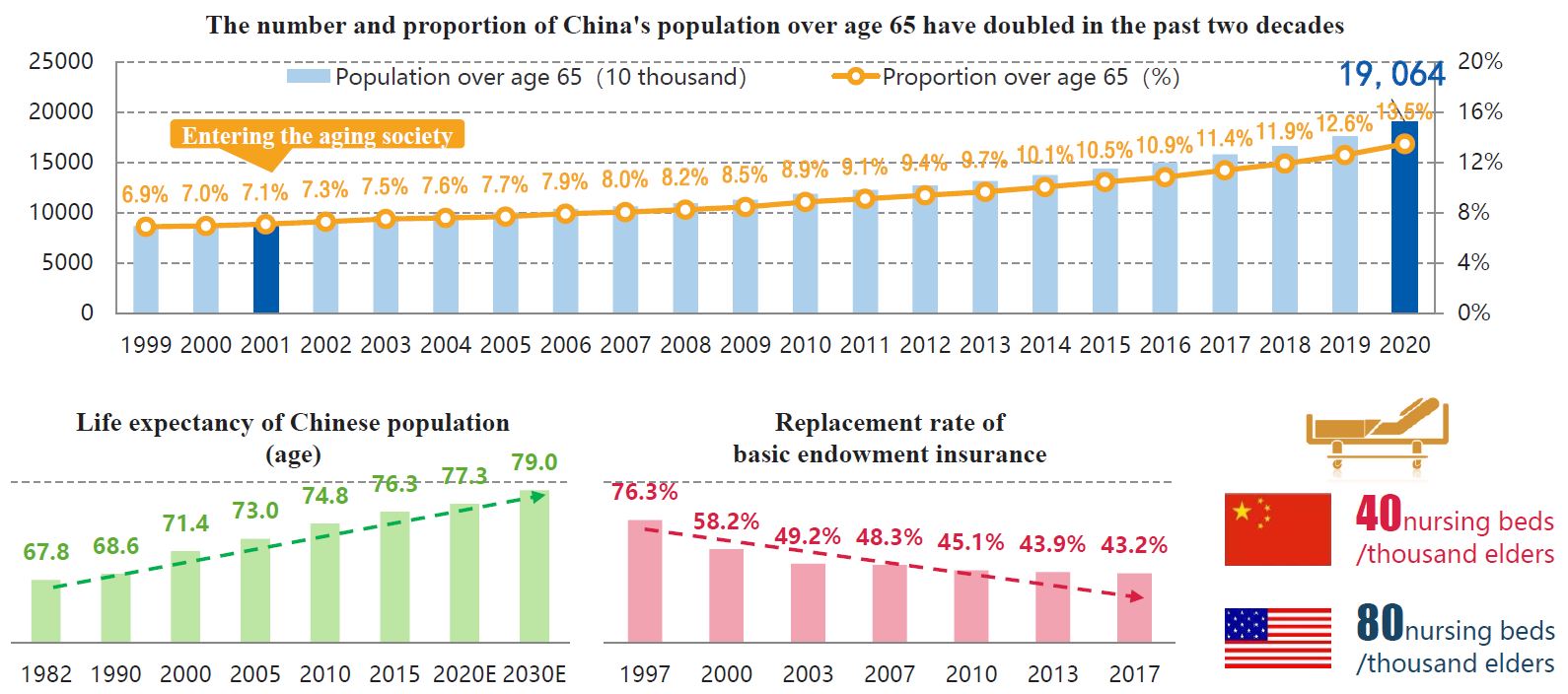

First, the age of longevity has put forth higher demands on the adequacy of China's pension and health reserves. Over the past 20 years, the number of people over 65 years of age in China has nearly doubled to more than 80 million. China is also set to enter an advanced stage of aging society ahead of time. The replacement rate of basic endowment insurance reached a historical peak of over 76%, while it is only around 44% at present.

Second, the coverage of institutional supplementary pensions is still relatively limited. While enterprise annuities continue to hover at less than 7% of the total, the proportion of institutional supplementary pension relative to the basic endowment insurance for urban workers has increased to 14% with the addition of occupational annuities. But overall, the proportion is still relatively limited, and further policy support and public enthusiasm are needed.

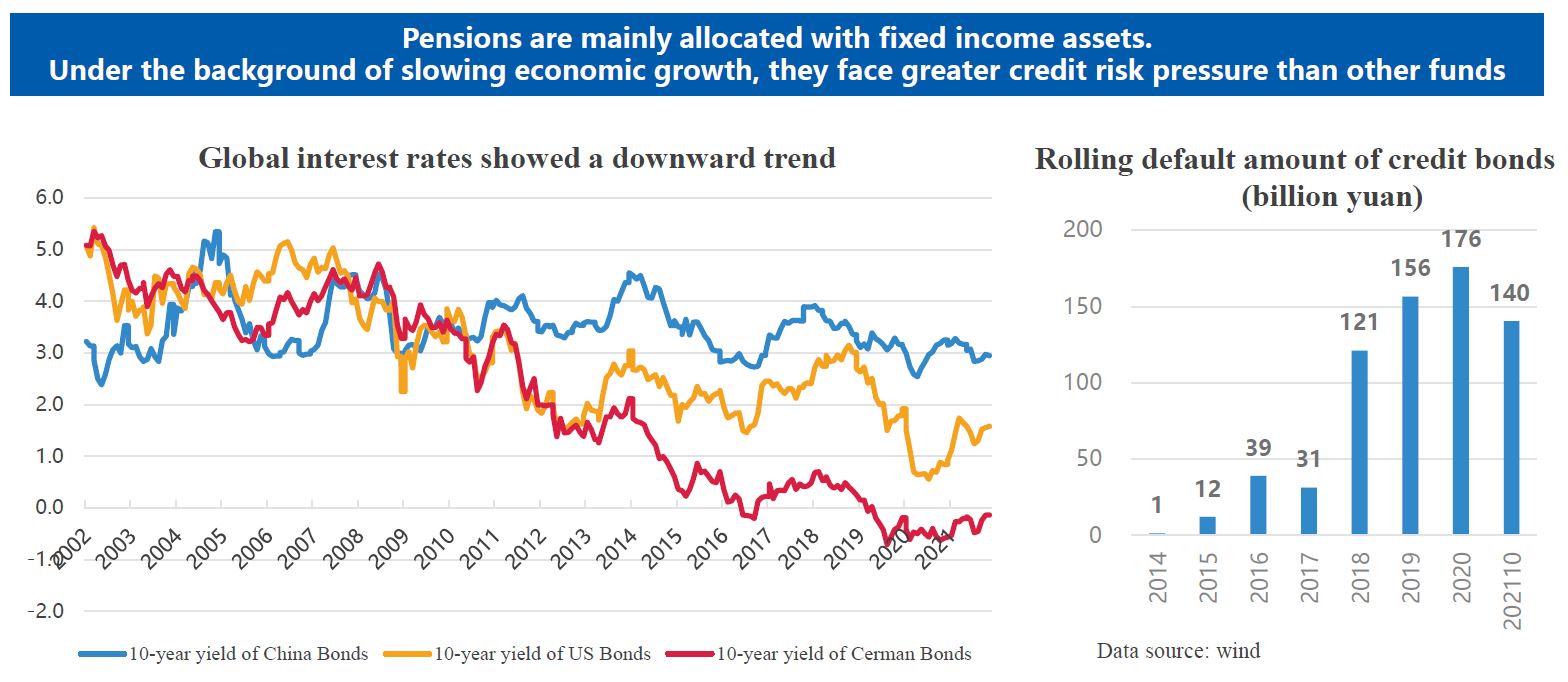

Third, credit risks continue to increase, putting cross-cycle asset allocation in pension management to the test. Out of security and stability considerations, pensions are still predominantly based on fixed income asset allocation. Therefore, in the context of slowing economic growth, pensions may face greater pressure from credit risks compared to other funds.

Reflections on the Paths To Promote the High-Quality Development of China’s Pension Market

From the institutional level, it is necessary to continuously optimize the three-pillar system. The first pillar should continue to promote the coordinated management at the national level to optimize the centralized management of provincial surplus funds and further enhance the investment efficiency and returns of basic pensions. For the second pillar, there is a need to significantly increase the participation rate, to actively explore automatic enrollment mechanisms with full consideration of the burden on enterprises and social equity, in combination with a long-term scientific annuity assessment mechanism and globalized asset allocation to improve the rate of return of annuities. For the third pillar, we should accelerate the establishment of a pension system based on individual commercial pension accounts and standardize the development of pension products that meet the requirements of the third system.

At the same time, there needs to be corresponding interactions and concerted initiatives among the three pillars. For example, exploring the mutual transfer of personal funds among the three pillars to increase the portability and flexibility of the pension accounts. And in the case of individuals who have not joined the second pillar, it may be possible for the corresponding tax credit to be superimposed on the third pillar to maximize the effect of tax preferential policies, as well as to establish a one-stop portal, combined with the operation of specialized institutions, to serve the second- and third-pillar businesses and enhance the pension experience of individuals.

At the market level, in July 2019, the General Office of the Financial Stability and Development Committee under the State Council announced 11 measures to open up the financial industry, allowing overseas financial institutions to invest and set up pension management companies with equity participation. This means that China's pension market will be facing a parallel model of "bringing in" and "going out." On the one hand, it will attract foreign institutions with professional pension management capabilities, while on the other hand, it will continue to promote the entry of China's pensions into the international capital market as well as its participation in global allocation.

We will also see the integration and cooperation between banks, insurance, securities, funds, and trusts continue to promote the synergy between pension wealth management, pension industry, pension fintech, community services, and medical and health management.

In terms of pension management institutions, we suggest accelerating the construction of an integrated retirement service ecosystem of pension and health, focusing on the needs of customers and providing customers with integrated plans to deal with longevity risks in long-term companionship.

In terms of the internal management of pension institutions, it is also important to accelerate the mutual integration of talent and technology, particularly the core trusteeship and investment management capabilities, and to promote technology to help unleash and solidify talents’ potential to the maximum.

How To Organically Integrate Pensions With the investment on ESG

A pension institution should also promote the organic integration of business model and social responsibility. This brings us to the topic under discussion today: How can pensions be integrated with the investment on ESG?

Pensions are managed over a long period of time and have very prominent social welfare attributes. These characteristics are highly compatible with the ESG investment philosophy of focusing on long-term value, taking into account of the interests of all parties, and reducing negative externalities.

On the investment side, ESG factors can be fully integrated into the investment decision and risk control system, and the managed funds can be invested in green industries in open or non-open markets.

On the product side, ESG-themed products can be developed to provide long-term financing to key projects with significant carbon emission reduction effects.

On the operation side, we can carry out green operations in an effective manner, guide shareholders and employees to participate, and create better economic benefits for beneficiaries by building up good reputation.

Of course, as long-term management funds, pension management requires the organic unity of long-term adherence and compliance risk control, as well as a positive interaction with the real economy.

In terms of capital investment, considering the long-term nature of pensions, it is necessary to synchronize capital investment with the country's overall development strategy, so as to achieve long-term steady returns through the cycle.

Guest Q&A

1. In the past decade, we have begun to face a variety of negative factors, such as an aging population, slow economic growth and climate change. Under such macroeconomic conditions, what are the challenges and opportunities for pension investment allocation?

In the context of increasingly aging population and climate risks, pension development is indeed facing huge challenges. The core issue of these challenges is the question of sustainability, for example, demographic changes will certainly lead to an imbalance in the overall social dependency ratio.

At the same time, as the issue of carbon neutrality gains increasing attention in the pension management industry against the backdrop of increased climate risks, attention will have to be paid to national policies in pension investment, and changes in the overall market as well as in technology could lead to potential losses in the value of carbon-intensive energy assets in our portfolios. At the same time, frequent natural disasters caused by climate change may also impact the industries we invest in.

Therefore, pension investments must be fully integrated with the philosophy of ESG investing to better adapt to the climate risk challenges posed on pensions, so that more long-term, sustainable and robust returns can be achieved for pensions.

2. In the attribution analysis of ESG investing performance, many evaluation results are actually incomplete, unreliable or relatively subjective. Are there specific measures on how pensions can contribute to sustainable investment on ESG?

In terms of ESG investing, we need to take a longer-term view on China’s pension assets. For example, how can we increase investment capacity on ESG?

First of all, it is necessary to improve the long-term management efficiency of service pensions, integrate investment on ESG into the use of pension in a more comprehensive manner, establish top-level design from the philosophy aspect to fully integrate with traditional pension asset allocation to form a more robust and high-quality green allocation plan.

Secondly, it is necessary to form a management system for investment on ESG, to integrate the green factors of ESG into the management and investment decision-making and risk control system, to accelerate the fundamental research on green industry by taking the long vision in order to promote the concept of green investment throughout the entire investment process of various assets. Of course, it also includes the formation of our quantitative index scoring system through external procurement of ESG data or self-built ESG data collection systems to provide reference for investment decisions.

In addition, the positive screening method should be more actively adopted to select the companies with the best ESG performance, best financial performance and best outlook among similar companies for analysis and investment. Of course, the exclusionary this strategy should also be strengthened to effectively eliminate the tail risks of some industries and individual companies under the double carbon background by improving policy prediction capabilities, so as to avoid substantial and significant pension investment risks.

3. According to the 2021 China Pension Outlook Survey Report by Fidelity and Ant Fortune, the funds’ capability in risk control and their philosophy in sustainable investment are the most important considerations for investors in choosing products, even greatly exceeding historical performance and brand effect. Is it true that investors have a relatively mature philosophy of ESG in the domestic financial product market? Are there any other trends in products you can share?

Since the beginning of this year, compounded by the impact of the pandemic, including the slowdown of global economic growth and the increase of uncertainties in the macroenvironment, credit risks continue to increase. Under these circumstances, people will certainly exercise more caution in pension investment, and also hope to find more stable investment targets.

In terms of long-term investment, a more robust investment style as such does not mean simply avoiding risks. For institutions, it is necessary to formulate asset allocation plans that are more effectively in line with investors’ objectives and tolerance over risks, and provide more effective long-term solutions.

Of course, we also need to keep up with the trend of increasing awareness of long-term investment and value investing, and effectively combine it with investors' focus on relevant new investment faCFctors, such as sustainability and ESG in order to create more cross-cycle returns for our clients.

In addition to paying more attention to investment risks, we will also see that the development of fintech and the construction of pension service ecosystems will also affect people's decision-making factors on pension investment.

Contactless financial services will play an increasingly important role in the future. Also in the future, the operation and management services of financial products for pensions will become more complex and sophisticated, and customer experience will have to be made simpler and more personalized. Therefore, the application of fintech will also change all aspects of our asset allocation, investment research, risk management and so on.

At the same time, based on the construction of the ecosystem, we need to create an all-round, all-scenario, full-coverage pension finance ecosystem for pension accumulation, investment, claim, product matching and supply of elderly care services, so as to provide better one-stop services for all. We also believe that the construction of these ecosystems will become a value-added service that everyone will inevitably consider for their pension investments.

Special thanks to Institutional Investor Review (IIR)’s Wang Qianying for this compilation.

The views expressed in this article are those of the author and should not be construed as investment advice, nor do they necessarily represent the views of the CFA Institute or the author's company. This article may not be reproduced in any form without authorization from CFA Institute.